Trader Tax Status: Learn How Traders Are Getting Taxed

Many traders focus on finding an edge in the market, seeking profitability and winning strategies, yet overlook how their trading income is taxed until problems appear. Trader tax status determines whether your profits are treated as investment returns or business income, directly affecting reporting, deductions, and legal compliance.

In this guide, you’ll learn how trading income is classified for tax purposes and how to manage taxes legally and responsibly as an active trader.

Key Takeaways

- Trader tax status determines how trading income is taxed: as investment gains or business income, affecting reporting and deductions.

- Tax classification depends on trading behaviour, not labels, helping active and funded traders avoid compliance mistakes.

What Is Trader Tax Status?

Trader tax status refers to how tax authorities classify an individual’s trading activity for tax purposes. It determines whether trading is treated as an investment activity or as a business, which directly affects how gains, losses, and expenses are reported for federal income tax purposes.

This distinction exists because traders do not all operate in the same way. Some trade occasionally for capital appreciation, while others engage in frequent trading aimed at profiting from short-term market movements.

A trader does not apply for trader tax status. Instead, tax authorities assess how trading activities are actually carried out. For example, a retail day trader trading their own capital, a trader operating a prop firm account, and a trader working within a hedge fund may all trade actively, yet be taxed differently. The difference lies in who owns the capital, how income is classified, and how profits are distributed.

How Trading Income Is Classified

Trading income is generally classified in one of two ways: investment-style treatment or business-style treatment. The classification depends on how trading activities are structured and executed, not on profitability alone.

Investment-Style Classification

Under an investment approach, traders seek capital appreciation over time through buying and selling securities held for profit. Positions are typically held longer, gains are treated as capital gains, while trading losses are subject to capital loss limitations. Investors generally have limited ability to deduct expenses, as trading is not considered an active business under the tax framework.

Business-Style Classification

When trading is frequent, continuous, and organised, tax authorities may treat it as a business activity. In this case, trading income is commonly classified as ordinary income rather than capital gains.

This classification may allow traders to deduct each qualifying trading expense incurred to produce income, but it also brings stricter reporting requirements and closer oversight by tax authorities under the applicable tax code in the United States.

Trading as a Retail or Individual Trader vs Trading as an Employee

The difference between trading as a retail or individual trader and trading as an employee is based on ownership of capital and income structure, not skill level or account size.

Trading as a retail or individual trader

A trader who trades their own account through a personal brokerage account is taxed based on how their activity is classified. Depending on trading frequency, structure, and intent, income may be treated as investment income or business income. This distinction applies equally to swing traders and high-frequency day trading participants.

Trading as an employee

A trader working for an investment bank or hedge fund trades capital owned by the firm or its investors. Compensation is taxed as employment income, while gains and losses belong to the firm and do not form part of the trader’s personal trading portfolio.

Prop Firm and Funded Trader Tax Status

Funded traders operate under a different tax framework than traders using their own capital because the trading account and capital belong to the prop firm, not the trader. Although trading activity may appear similar, the legal and tax treatment differ because the trader is not investing personal funds.

In the United States, payouts from funded trading arrangements are generally treated as ordinary income rather than capital gains. Trading gains and losses generated within the prop firm account belong to the firm and are not reported by the trader; only the payouts received under the contractual agreement are taxable, typically at marginal income tax rates, which may be higher than long-term capital gains rates.

Indicative U.S. tax treatment for funded traders

In the U.S., funded trader payouts are generally treated as ordinary income, with the overall tax burden depending on how the income is classified and where the trader resides:

- 25%–35% total → if subject to federal income tax plus state tax

- 30%–45% total → if federal tax, state tax, and self-employment tax apply, depending on income, structure, and state

Looking for a trusted prop firm?

Top One Trader is a legitimate proprietary trading firm that provides a transparent funding model, clear trading rules, and fast payouts, giving traders everything they need to trade funded accounts with confidence.

How Tax Authorities Determine Trader Status

Tax authorities determine trader status based on actual trading behaviour rather than stated intention. There is no single test; instead, several factors are evaluated together.

Common considerations include the frequency and dollar amount of trades, typical holding periods, the time devoted to trading, and whether the activity shows continuity and regularity. A focus on daily market movements rather than long-term investment returns supports a trading classification.

Authorities may also examine whether trading is conducted through a separate brokerage account, whether detailed records are maintained, and whether the activity is organised in a business-like manner. Trader status is determined by the overall pattern of activity.

Trader Tax Status: Benefits and Limitations

Trader tax status is not about chasing tax benefits, but about aligning tax treatment with how trading is genuinely conducted. When trading qualifies as a business, it reflects active market participation while adding compliance responsibilities.

Benefits for Active Traders

When trading is classified as a business activity, traders may be able to deduct certain ordinary and necessary expenses directly related to producing trading income. These deductions are not available to passive investors and must be properly documented.

Common examples include:

- Trading software, platforms, and market data subscriptions

- Education and research are directly related to trading activities

- Office space used exclusively for trading

- Professional services related to tax reporting or compliance

In the United States, some traders who qualify as operating a trading business may also be eligible to make a mark-to-market election under Section 475(f), which applies to securities and other securities defined under federal rules.

Limitations to Consider

Mark-to-market rules can increase taxable income in years where open positions show unrealized gains, even if those positions have not been closed. Once elected, this accounting method can be difficult to reverse and should be evaluated carefully despite the potential tax benefits it may offer under certain conditions.

Traders classified as operating a business under trader tax status (TTS) are also subject to greater scrutiny from tax authorities. Detailed record-keeping and a clear separation between trading and investing activity are essential. Trader tax status is not a shortcut; it must be supported by disciplined and well-documented behaviour.

Common Tax Mistakes Traders Make

Many tax issues arise not from complexity, but from incorrect assumptions. Traders often treat taxes as an afterthought, which can lead to avoidable problems.

Some of the most common mistakes include:

- Assuming all trading gains are capital gains, regardless of activity level

- Misunderstanding how funded trading income should be reported

- Mixing trading and investment activity in the same account

- Ignoring wash sale rules when trading frequently

- Failing to report gains and losses accurately on the tax return

These issues are especially common among day trading participants who increase activity without adjusting their tax approach. As trading frequency grows, the tax implications become more complex and require more structure.

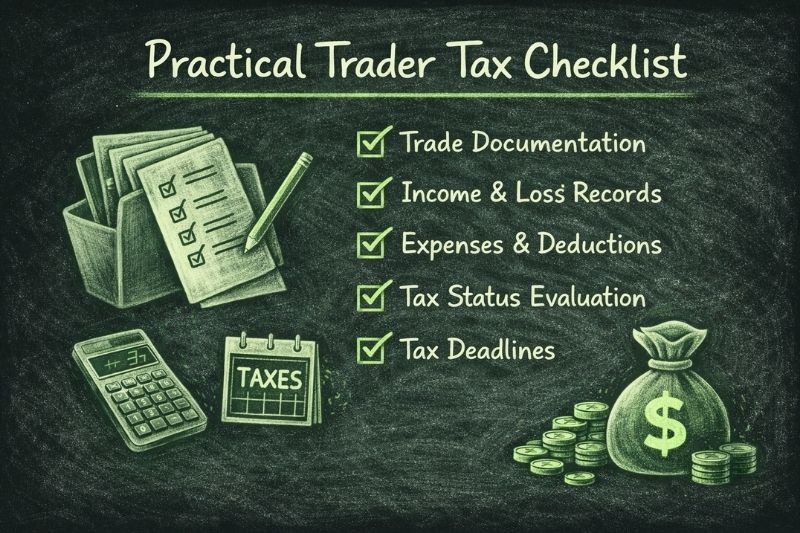

Practical Trader Tax Checklist

The checklist below helps traders assess whether their current approach aligns with their tax status and trading behaviour.

Final Thoughts

Trader tax status is not about labels or loopholes. It reflects how seriously and systematically a trader engages with the market. As trading evolves from occasional activity into a structured business, tax treatment must evolve alongside it.

Professional traders understand that taxes are part of the overall risk framework. Just as poor risk management can undermine trading performance, poor tax planning can undermine long-term results. Clarity, discipline, and accurate reporting are essential at every stage.

Ready to become a profitable trader?

Top One Trader supports traders who value discipline, transparency, and long-term consistency, offering clear rules, competitive pricing, fast payouts, and educational support to help you achieve your goals.

-1%201%20(1).webp)